Monday, June 29, 2009

Saturday, June 27, 2009

Microfinance and the Recession

A story from the East African, reporting that many microfinance institutions are facing tougher economic conditions.

Saturday, June 20, 2009

Microfinance course readings PAD 612

PAD 612 Nonprofits and Public Policy, Spring 2008

Rockefeller College of Public Affairs and Policy

Instructor: Erzsebet Fazekas

International Development: Public Policy Objectives, Market Tools and Nonprofit Action

Forman, Shepard and Abby Stoddard. 2002. “International Assistance.” Pp. 240-274 in The State of Nonprofit America.

Smith, Brian H. 1998. “Nonprofit Organizations in International Development: Agents of Empowerment or Preservers of Stability?” Pp. 217-227 in Private Action and the Public Good edited by Walter W. Powell and Elisabeth S. Clemens. New Haven: Yale University Press.

The Case of Microfinance

Morduch, Jonathan and Beatrix Armendariz. 2004. “Microfinance: Where do we stand?” in Financial Development and Economic Growth: Explaining the Links edited by Charles A. E. Goodhart. New York: Palgrave Macmillan. ERes

Bruck, Connie. 2006. “Millions for Millions.” The New Yorker, October 30, 2006. 8

Review the websites of Grameen Foundation <> and Kiva.

Rockefeller College of Public Affairs and Policy

Instructor: Erzsebet Fazekas

International Development: Public Policy Objectives, Market Tools and Nonprofit Action

Forman, Shepard and Abby Stoddard. 2002. “International Assistance.” Pp. 240-274 in The State of Nonprofit America.

Smith, Brian H. 1998. “Nonprofit Organizations in International Development: Agents of Empowerment or Preservers of Stability?” Pp. 217-227 in Private Action and the Public Good edited by Walter W. Powell and Elisabeth S. Clemens. New Haven: Yale University Press.

The Case of Microfinance

Morduch, Jonathan and Beatrix Armendariz. 2004. “Microfinance: Where do we stand?” in Financial Development and Economic Growth: Explaining the Links edited by Charles A. E. Goodhart. New York: Palgrave Macmillan. ERes

Bruck, Connie. 2006. “Millions for Millions.” The New Yorker, October 30, 2006. 8

Review the websites of Grameen Foundation <> and Kiva.

Kiva Community Conference Call

Every month we hold an open conference call as an open forum for lenders and Kiva staff to talk about what's going on. Please join us for our next call, scheduled for Wednesday, July 15th at 2 pm PDT.

The call in info is:

Dial in US: 866-740-1260

Dial in (Outside US): +1 303-248-0285

Access Code: 6415483

We hope to hear you on the line!

Source: Inside Kiva - http://www.kiva.org/

The call in info is:

Dial in US: 866-740-1260

Dial in (Outside US): +1 303-248-0285

Access Code: 6415483

We hope to hear you on the line!

Source: Inside Kiva - http://www.kiva.org/

Monday, June 15, 2009

Summary of Lending to Date

Total Amount Lent = $575

Total Amount Repaid = $4

Amount of Ended Loans Defaulted = $0.00

Amount of Ended Loans = $0.00

Default Rate = 0.00%

Delinquency Rate = 0.00%

Total Amount Repaid = $4

Amount of Ended Loans Defaulted = $0.00

Amount of Ended Loans = $0.00

Default Rate = 0.00%

Delinquency Rate = 0.00%

Loan to Celia Morales for her restaurant

We loaned $25 to Celia Morales in Bolivia.

Celia has a “pensión” (small restaurant) where she sells “chicharrón” (crispy, fried chicken and pork rinds). She works with one employee. This business helps her to be able to pay her food expenses.

She lives in the Villa Copacabana zone, Escobar Uria sector, city of La Paz. The loan is to buy tables and chairs for her pensión.

This is the third time she has asked for a loan from Impro, and the second time she has needed help from Kiva. Her desire to improve herself has given her the opportunity to be eligible for this loan.

Loan to Candida Rosa Méndez in Nicaragua

We loaned $25 to Candida Rosa Méndez:

In the city of Chinandega, Ms. Candida Méndez sells shoes at her own business that she has attended to for 35 long years. This business has permitted her to grow and receive an income.

She has found it necessary to expand, and has therefore turned to CEPRODEL to be a beneficiary of credit to purchase footwear to fill her shelves and offer a variety of footwear to the public, so she can continue making an income to support her household.

Loan to Almas Group in Tanzania

We have loaned $100 to the Almas Group:

Salma Ally, age 30, is single with no child. She sells clothes from her home and also door to door. She started this business in 1968 and works from 10 a.m. to 4 p.m. daily. She is able to earn a monthly profit of about $114.

This will be Salma’s 6th loan from Tujijenge Tanzania. She used the previous loans to increase her clothing business, bought house furniture, bought land and has paid back her loans successfully. She hopes to get her 6th loan to increase her capital and to buy bricks.

Salma will share this loan with her group, Almas, which totals twenty-two members. These members will hold each other accountable in paying back their loans. In the picture, Salma is second from the left in a black blouse and yellow skirt.

Loan to Mercedes del Carmen Avendaño Perez

The latest loan is $150 to Mercedes del Carmen Avendaño Perez in Nicaragua. She lives in Managua with her parents, where she studies and works in agriculture. She has been doing this work for the past five years, but wants the loan to buy fertilizers for her crop. You can view her profile here.

Field Report: CreditMujer/Manuela Ramos, Peru

Following on from my last post, I have received this field update from Kiva fellows in Peru:

Manuela Ramos is an organization dedicated to the advancement of Peruvian women. Founded in 1978, its programs include educating women, primarily in the rural areas of Peru, about gender equality, domestic violence, women’s rights and environmental awareness. It now has programs in fifteen locations throughout Peru, with seven regions operating microfinance programs. The microfinance program on which we worked, CrediMujer, assists groups of 15-30 women to come together, form a community bank, and take out a loan to use in their individual businesses. This is where Kiva comes in, by providing interest-free capital for Manuela Ramos to lend.

By supporting an entrepreneur who works with Manuela Ramos/CrediMujer, you are also supporting the progress of women living in the poorest regions of Peru. Although the loan amounts offered by Manuela Ramos are small (between $100 and $1,000), they make an impact on these women’s lives by providing them with the necessary capital to start and, sometimes, to expand their businesses.

Entrepreneurs partake in different businesses depending on the regions in which they live. Our experiences as Kiva Fellows in the field have also been influenced by the diverse geography in Peru. In the San Martin region, which is located in the Amazon basin of Peru, Diana encountered not only some very hot days, but also the warmth and generosity of its women, who would often give her treats like coconut water, fresh oranges, and cold soft drinks to help her cool off after a long day walking under the sun. Because San Martin's primary economic activity is agriculture, Diana visited many entrepreneurs with businesses related to agriculture or food production and sales. Growing cocoa, selling plantains, preparing local dishes like juanes (a mixture of rice, chicken, eggs, olives, and spices, wrapped in "bijao" plant leaf) and anticuchos (grilled meat on a skewer), and selling basic foods, were the most common business activities in this area.

In the city of Puno, nestled in the Peruvian Andes, Emily experienced the bitter cold and intense sun that the region is known for and saw the economic benefits that the tourism industry has brought to the area.

Puno is located on the shores of Lake Titicaca, the highest navigable lake in the world, and attracts many tourists who buy Peruvian tapestries, embroideries and alpaca sweaters, scarves and hats to keep warm. In addition to creating these artesian goods to sell to tourists, many Manuela Ramos entrepreneurs work in businesses that fatten livestock and operate small kiosks or general food stores.

Although we have been working separately in two different Manuela Ramos offices, we have focused on the same type of work, primarily writing journals for Manuela Ramos’s Kiva entrepreneurs. While the borrower profiles on Kiva’s site present information about how the entrepreneur plans to use the loan, journals provide follow-up information about how that loan was used and the effect it has had on the entrepreneur’s life. Although Manuela Ramos has employees and Kiva Fellows like us working hard to increase the number of journals written, financial and logistical constraints make it very difficult to produce a journal for each entrepreneur. Whether or not you have received a journal about the Manuela Ramos entrepreneur to whom you gave a loan, we hope that you will enjoy the story of Gloria, one of these entrepreneurs.

Gloria lives in the city of Tarapoto, the main commercial hub of the San Martin region. She makes “salchipapas,” a dish consisting of French fries and hot dog links, often accompanied by coleslaw or other variations, depending on the cook's particular style. Gloria's love for her business shows not only in the quality of her service and the food she serves, but also in her loyal customer base. Gloria has been a member of her community bank for quite a few years and her most recent loan of 1,000 soles (approximately $300 USD), was financed through Kiva by lenders like you. With this loan, Gloria bought tables, chairs and other supplies. This investment allowed her to better serve her customers and provide them with a more comfortable environment. However, Gloria's plans for her business don't end there. As an enterprising woman, she is thinking about the future of her business. To hear more about these plans from Gloria, see this short video interview (scroll to the bottom of the page).

Thank you for supporting entrepreneurs like Gloria and helping Manuela Ramos work on behalf of Peruvian women!

Best Regards,

Emily Sweeney and Diana Rodriguez

Kiva Fellows 7th Class

Field Report: Emprender in Bolivia

Kiva hires a number of fellows to report on progress with various lending projects. I received this report today from a Kiva fellow working with Emprender in Peru, one of the organizations that we have loaned through:

"I have been working as a Kiva Fellow in Emprender’s offices for the past 3 months, and have been greatly impressed with the high quality of their staff, their commitment to the people in their community, and unique services they offer their clients.

In particular, Christian Rivera should be recognized for his work. He is Emprender’s Kiva Coordinator. He posts profiles of Emprender clients on the website for Kiva lenders to fund, keeps in touch with both lenders and Kiva staff, and helps to make sure Emprender staff understands and participates in Kiva in the best, most effective way possible.

Christian has been wonderful in this position, but will soon be passing the responsibility to another Emprender staff member, Jose Luis.

Christian plans to focus his attention on a unique project that Emprender is starting. He is also a doctor, and has organized a medical program for Emprender clients.

Sadly, Bolivia has the worst health conditions in South America and is second only to Haiti in the hemisphere. In an effort to improve the health and well being of their society, Emprender, with the help of the Center for the Sustainable Development (CEDESS) and An Ber, will open free clinics for their clients and offer medical treatment at reduced costs for the members of client families. The clinics will be located within Emprender offices, making access convenient and efficient. They will even offer medical services for other community members in semi-urban and rural areas that are under-serviced by other medical facilities. These clinics will provide basic and preventative medicine, family planning, and other health education services. The first of the six clinics will open within the next three months, as soon as the final paperwork has been completed. Emprender hopes to reach 50% of their clients by the end of the first year, and 100% of their clients by the third year of the project. In addition to organizing the project, Christian will be the doctor at Emprender’s first clinic. I am constantly impressed by his ability to wear many hats and know he looks forward to this transition in his job.

It is everyone’s hope that by providing medical services, Emprender’s borrowers won’t face financial disaster caused by preventable illness. Ideally, these medical services will improve the lives of Emprender’s borrowers, increase their repayment capacity, and help inoculate the family from medical risk.

I saw first hand the ways that simple medical treatment could help an Emprender client. Alejandra and her husband Demecio purchase, raise, and then sell ducks in the small town of El Torno outside of Santa Cruz, Bolivia, where Emprender has a field office. Alejandra has been selling ducks for over 20 years, and often has more than 70 ducks in her yard at a time. With the income from her and Demecio’s business, they are raising their 8 children. Unfortunately, a few weeks before I met Alejandra, she stepped on a piece of glass that cut her foot. Perhaps from working so close to animals, or perhaps due to just bad luck, the cut got infected. The infection has grown and grown and Alejandra has had trouble walking, and now spends most of the day off her feet. Her business is suffering, because she can make fewer trips each week to the market to sell, and is reliant on people coming to her home to purchase ducks. Emprender hopes to be able to help its clients by providing basic medical care that can help them feel better and continue to succeed in their businesses.

It has been a pleasure for me to get to know Emprender’s staff across the country and to learn about the many ways in which this socially focused organization provides for its clients — Kiva borrowers.

Thank you again for lending to Emprender’s clients and for believing in the power you have to make a difference. Gracias!

Sincerely,

Sierra Visher

Kiva Fellow"

Wednesday, June 10, 2009

The Reith Lectures 2009: Markets and Morals

The Reith Lectures are an annual series of public lectures hosted by the BBC.

The first lecture from this year's series is particularly relevant for microfinance - titled "Markets and Morals", given by Michael Sandel, Professor of Government at Harvard. You can listen to the lecture here.

The first lecture from this year's series is particularly relevant for microfinance - titled "Markets and Morals", given by Michael Sandel, Professor of Government at Harvard. You can listen to the lecture here.

Sachs-Poyo-Easterly: Who will win the aid debate?

There appear to be some heated arguments flying around (as reported by Kristi York Wooten at the Huffington Post) over the future of aid policy between some of the big guns: Jeff Sachs (economist at Columbia), William Easterly (at NYU) and relative newcomer, Dambisa Moyo (author of the book Dead Aid). Easterly sums up the debate here on his blog.

Moyo's book makes some strong accusations of the aid 'establishment': namely, that aid to Africa has created dependency on the West. The book has made a big splash in the media world - enough for Time magazine to name her as 'one of the most influential 100 people in the world'...

Moyo's book makes some strong accusations of the aid 'establishment': namely, that aid to Africa has created dependency on the West. The book has made a big splash in the media world - enough for Time magazine to name her as 'one of the most influential 100 people in the world'...

Jaime Pozuelo-Monfort on Microfinance

Jaime Pozuelo-Monfort: Words Apart

from Breaking News and Opinion on The Huffington Post by Jaime Pozuelo-Monfort

"On Sunday night I had dinner with World Bank economist Branko Milanovic, one of the leading experts in income inequality. Branko authored a book in 2005 called Worlds Apart. It is after Branko's inspiring book that this article is entitled. Branko's book describes the immense income gap between Hemispheres. This article describes the immense opinion gap when it comes to approaching the eradication of extreme poverty.

This morning I met with Elizabeth Littlefield, the Chief Executive Officer of the Consultative Group to Assist the Poor (CGAP). This afternoon I am meeting with the Malagasy Ambassador to the United States Jocelyn Radifera. Overall I have conducted 210 phone interviews and 270 face to face interviews in preparation for the writing of my forthcoming book. I have discussed the future of microfinance with some of the experts in the field that include Maria Otero (Accion), Michael Chu (Harvard Business School), Chuck Waterfield (Microfin), Hugh Allen (VSL Associates), Kim Wilson (Tufts), Dean Karlan (Yale), Jonathan Zinman (Dartmouth), Jonathan Morduch (NYU), Chris Dunford (Freedom from Hunger), Alex Counts (Grameen Foundation), Carlos Danel (Compartamos), Maria Nowak (Adie), Shabbir A. Chowdhury, Aminul Alam and Imran Martin (BRAC), Lamiya Morshed and Nurjahan Begum (Grameen), Premal Shah (Kiva), Sam Daley-Harris and Bob Sample (Results), Adrian Gonzalez (Microfinance Exchange Network), Ann Rutledge (R&R Consulting), Michael McCord (Microinsurance Centre), In Channy (ACLEDA Bank), Lynne Patterson and Irina Aliaga (Promujer), Niki Armacost (Women's World Banking), Martha Chen (Harvard) and Matt Bannick (Omydiar Network).

I approached the microfinance industry in the same manner that I have approached other areas such as agriculture, trade and labour rights, financial architecture, immigration, small arms trade and military spending or the mining industries. I sampled the industry and tried to reach out the most relevant experts. I have seen words apart. A majority of the experts on the microfinance industry are not on the same page. Some of the following questions may be familiar to the reader: how can microcredit penetration be expanded among the bottom billion? Is Compartamos the right approach to banking for the poor? Has microcredit being emphasized over microsavings? What role do innovators such as Kiva.org play in the field? Should microfinance institutions receive subsidies from national agencies and foundations? What are the Omydiar Network and the Gates Foundation doing to enhance basic financial services for the poor? What is the impact of the World Bank and the United Nations' involvement in microfinance?

Not everyone is on the same page. Is there a same page? Do you agree with Muhammad Yunus and Hernando de Soto? The overlap of opinions is manifest. There is an intellectual debate which could be healthy, but it oftentimes ends up in intellectual wars that forsake the ultimate goal: the alleviation of extreme poverty. If poverty is not eradicated it is not only because of a lack of political will or interest among developed nations and the elites of the developing world. Poverty is not eradicated because there is a lack of consensus as to how to mitigate it. The intellectual wars of left-wing and right-wing economists and practitioners do not help. The debate between what approach is more appropriate (for instance between USAID and the Millenium Challenge Corporation) perpetuates the problem. It is difficult to get everyone on the same page. What is that same page? There are many possibilities, but only one will materialize if a global effort is to be undertaken to create a new architecture for the extreme poor that sets once and for all the basis for the eradication of extreme poverty.

We have been born in a world that adores criticism in an area where the lack of innovation is second to none. We are all sports journalists broadcasting a football game that has been going on for decades. There is an abundance of commentators and a scarcity of implementators.

For decades social scientists have been elaborating theories that had no direct application. Humans built a first architecture in the aftermath of World War II, it is called the Bretton Woods architecture. For decades we as a society were reluctant to build a second architecture. We have not looked at the best ideas in the development arena from intellectual giants such as Jeffrey Sachs, Dani Rodrik, William Easterly, Paul Collier or Hernando de Soto. The de facto approach has been to channel funds through the existing schemes. There are recent pilots that are promising such as the Millenium Challenge Corporation.

What is the next big idea in the development space? Sampling the universe of opinions in the microfinance industry can only be helpful. The experts mentioned beforehand may or may not agree on how to tackle extreme poverty through microcredit, microsavings and microinsurance. There is one fact. Only when the experts become expert dreamers, only when the experts become men and women of stature will we be eyewitnesses of the birth of a new consensus, a new architecture that is designed to work for the extreme poor. It is perhaps time to propose a page one to start the Glorious Forty that will lead us to the world of cornucopia and eutopia. It is perhaps time to start a journey where only dreamers are welcome. It is perhaps time to start saying why not instead of why. We must dare, therefore we exist."

from Breaking News and Opinion on The Huffington Post by Jaime Pozuelo-Monfort

"On Sunday night I had dinner with World Bank economist Branko Milanovic, one of the leading experts in income inequality. Branko authored a book in 2005 called Worlds Apart. It is after Branko's inspiring book that this article is entitled. Branko's book describes the immense income gap between Hemispheres. This article describes the immense opinion gap when it comes to approaching the eradication of extreme poverty.

This morning I met with Elizabeth Littlefield, the Chief Executive Officer of the Consultative Group to Assist the Poor (CGAP). This afternoon I am meeting with the Malagasy Ambassador to the United States Jocelyn Radifera. Overall I have conducted 210 phone interviews and 270 face to face interviews in preparation for the writing of my forthcoming book. I have discussed the future of microfinance with some of the experts in the field that include Maria Otero (Accion), Michael Chu (Harvard Business School), Chuck Waterfield (Microfin), Hugh Allen (VSL Associates), Kim Wilson (Tufts), Dean Karlan (Yale), Jonathan Zinman (Dartmouth), Jonathan Morduch (NYU), Chris Dunford (Freedom from Hunger), Alex Counts (Grameen Foundation), Carlos Danel (Compartamos), Maria Nowak (Adie), Shabbir A. Chowdhury, Aminul Alam and Imran Martin (BRAC), Lamiya Morshed and Nurjahan Begum (Grameen), Premal Shah (Kiva), Sam Daley-Harris and Bob Sample (Results), Adrian Gonzalez (Microfinance Exchange Network), Ann Rutledge (R&R Consulting), Michael McCord (Microinsurance Centre), In Channy (ACLEDA Bank), Lynne Patterson and Irina Aliaga (Promujer), Niki Armacost (Women's World Banking), Martha Chen (Harvard) and Matt Bannick (Omydiar Network).

I approached the microfinance industry in the same manner that I have approached other areas such as agriculture, trade and labour rights, financial architecture, immigration, small arms trade and military spending or the mining industries. I sampled the industry and tried to reach out the most relevant experts. I have seen words apart. A majority of the experts on the microfinance industry are not on the same page. Some of the following questions may be familiar to the reader: how can microcredit penetration be expanded among the bottom billion? Is Compartamos the right approach to banking for the poor? Has microcredit being emphasized over microsavings? What role do innovators such as Kiva.org play in the field? Should microfinance institutions receive subsidies from national agencies and foundations? What are the Omydiar Network and the Gates Foundation doing to enhance basic financial services for the poor? What is the impact of the World Bank and the United Nations' involvement in microfinance?

Not everyone is on the same page. Is there a same page? Do you agree with Muhammad Yunus and Hernando de Soto? The overlap of opinions is manifest. There is an intellectual debate which could be healthy, but it oftentimes ends up in intellectual wars that forsake the ultimate goal: the alleviation of extreme poverty. If poverty is not eradicated it is not only because of a lack of political will or interest among developed nations and the elites of the developing world. Poverty is not eradicated because there is a lack of consensus as to how to mitigate it. The intellectual wars of left-wing and right-wing economists and practitioners do not help. The debate between what approach is more appropriate (for instance between USAID and the Millenium Challenge Corporation) perpetuates the problem. It is difficult to get everyone on the same page. What is that same page? There are many possibilities, but only one will materialize if a global effort is to be undertaken to create a new architecture for the extreme poor that sets once and for all the basis for the eradication of extreme poverty.

We have been born in a world that adores criticism in an area where the lack of innovation is second to none. We are all sports journalists broadcasting a football game that has been going on for decades. There is an abundance of commentators and a scarcity of implementators.

For decades social scientists have been elaborating theories that had no direct application. Humans built a first architecture in the aftermath of World War II, it is called the Bretton Woods architecture. For decades we as a society were reluctant to build a second architecture. We have not looked at the best ideas in the development arena from intellectual giants such as Jeffrey Sachs, Dani Rodrik, William Easterly, Paul Collier or Hernando de Soto. The de facto approach has been to channel funds through the existing schemes. There are recent pilots that are promising such as the Millenium Challenge Corporation.

What is the next big idea in the development space? Sampling the universe of opinions in the microfinance industry can only be helpful. The experts mentioned beforehand may or may not agree on how to tackle extreme poverty through microcredit, microsavings and microinsurance. There is one fact. Only when the experts become expert dreamers, only when the experts become men and women of stature will we be eyewitnesses of the birth of a new consensus, a new architecture that is designed to work for the extreme poor. It is perhaps time to propose a page one to start the Glorious Forty that will lead us to the world of cornucopia and eutopia. It is perhaps time to start a journey where only dreamers are welcome. It is perhaps time to start saying why not instead of why. We must dare, therefore we exist."

Liliam Nunez de Souza, Peru

"Liliam Nunez de Souza lives in the city of Pucallpa and is a member of the communal bank called Las Gemas II. She is 47 years old and has three grown children. Her husband sells beverages for work. She began her business selling beauty products and perfumes through catalogs. With her first loan, she purchased a small display case to show her products. Liliam is a pharmacy technician and her business has been growing. In parallel to her investment in selling beauty products, she also works together with her family selling medicines.

To date, medicine sales have improved and have increased sales, and now she needs more capital to invest in cosmetics, perfumes as well as more medicine. She says that Manuela Ramos has given her many opportunities to work together with her family, not only providing a source of income, but uniting them in improving their quality of life."

Monday, June 8, 2009

Ngorogoro Group in Tanzania

James Manyama, age 30, is married with two children, ages six and three and a half months. He has a furniture mart business which he started three years ago. He works daily from 7am until 7pm and he is able to earn a monthly profit of around $746.

This will be James’s sixth loan from Tujijenge Tanzania. He used the previous loans to increase his business by buying more wood for his furniture business. He has paid back his loan successfully. He wants a new loan to increase his capital to buy more materials, like leather for sofa sets and vanish for wood.

James will share this loan with his group, "Ngorongoro" which totals 18 members. Members will hold each other accountable for paying back their loans. In the picture, James is second from right, in blue.

This will be James’s sixth loan from Tujijenge Tanzania. He used the previous loans to increase his business by buying more wood for his furniture business. He has paid back his loan successfully. He wants a new loan to increase his capital to buy more materials, like leather for sofa sets and vanish for wood.

James will share this loan with his group, "Ngorongoro" which totals 18 members. Members will hold each other accountable for paying back their loans. In the picture, James is second from right, in blue.

Latest Lending

Our latest lending!

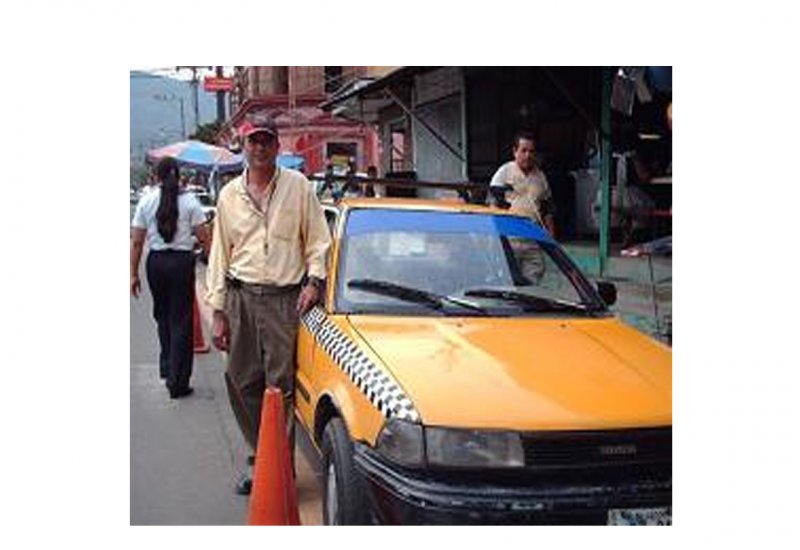

"Rosalio Rafailan de Paz is 48 years old, and lives in Nueva San Salvador with his wife and their three young children, who are in school. He works as a taxi driver and owns his own vehicle. Rosalio is a very respectful man who makes sure that he provides good service to his customers. Rosalio performs complete maintenance on his taxi every year so that his taxi service will be safer. It is for this reason that Rosalio is asking for a loan, which he will use to purchase new parts for his automobile."

"Rosalio Rafailan de Paz is 48 years old, and lives in Nueva San Salvador with his wife and their three young children, who are in school. He works as a taxi driver and owns his own vehicle. Rosalio is a very respectful man who makes sure that he provides good service to his customers. Rosalio performs complete maintenance on his taxi every year so that his taxi service will be safer. It is for this reason that Rosalio is asking for a loan, which he will use to purchase new parts for his automobile."

Thursday, June 4, 2009

The Role of Women in Poverty Redution- World Bank

This is an article that details the importance of women in poverty-reduction in developing countries. It explains the importance of equality in education and their participation in the economic sector. It also asserts that the benefits of targeting women and girls for eco participation extends beyond women to the society at large.

READ:

http://www1.worldbank.org/prem/PREMNotes/premnote128.pdf

READ:

http://www1.worldbank.org/prem/PREMNotes/premnote128.pdf

Tuesday, June 2, 2009

Papers from the Grameen Foundation

The Grameen Bank in Bangladesh is considered to be a pioneering microfinance institution:

The Grameen Foundation, a related organization, has a series of interesting papers on its web site that are worth a look.

"Started in 1976 by Professor Muhammad Yunus with a mere $27 from his own pocket, Grameen Bank today serves more than six million poor families with loans, savings, insurance and other services. The bank is fully owned by its clients and has been a model for microfinance institutions around the world."

The Grameen Foundation, a related organization, has a series of interesting papers on its web site that are worth a look.

Microfinance Best Practice Resources

A series of best practice papers from the Small Enterprise Education and Promotion (SEEP) Network, an organization in Washington DC which provides training and guidance for microfinance institutions.

Kiva on Frontline

The Frontline World site has a video examining Kiva's operations in Uganda, as well as some first hand accounts from lenders and interviews with the Kiva staff.

Why is microfinance weak in Africa?

In this story from Voice of America Mary Ellen Iskenderian of Women’s World Banking discusses her organization's recent diagnostic of microfinance in Africa.

The report finds that

and highlights high costs caused by low population density and poor infrastructure and a lack of skilled managers as key constraints on the penetration of microfinance.

The report finds that

"...the current market penetration to low-income households is

less than 15 percent for savers and even lower for borrowers..."

and highlights high costs caused by low population density and poor infrastructure and a lack of skilled managers as key constraints on the penetration of microfinance.

Microsavings? NYT Blog Post

This blog post from Nicholas Kristof argues that microlending should be supplemented by microsaving.

"many poor people must pay to save. That’s right — instead of receiving interest for depositing their savings with someone, they have to pay interest on their own money. One common scheme in West Africa, for example, charges an annual interest of 40 percent for accepting savings."

Another recipient group

$25 contribution to the Suraiya Abdul jabbar Group in Vehari, Pakistan. The four women in the group plan to use the loan to buy a sewing machine, to buy vegetables to resell, buy sugarcanes to sell their juice and to buy books to sell in a book store.

What we did, part II - RPOS572 Spring 2009

RPOS 572: Rockefeller College Microfinance Initiative

What we did and why we did it

The Rockefeller College Microfinance Initiative began as an idea generated from the Spring 2009 Foreign Economic Policy class. The challenges of development and the hardships of global poverty inspired a drive to get involved as a unit, as well as on behalf of the College. While noting its shortcomings, the class elected to get involved in microfinance and the decision was made to use Kiva.org as the institution through which the investment would be made. The microfinance or micro loan model of aid has a much different structure to foster a higher standard of living for individuals living in poverty. These programs provide money, but in the form of loans rather than goods or services. These loans are given to entrepreneurs that can use the money to invest in their own production capacity. They invest in projects ranging from business investment for expansion, agricultural production, or whatever project that will generate income so that the loan can be repaid and passed on to the next project. Thus, Kiva was a good fit for our initiative. One of the best traits of microfinance projects is that the individuals involved are in charge of their own destiny. They are taking on risk, just the same as the donor is taking a risk of not having their loan repaid. There are also added benefits of bypassing many government agencies that could potentially divert funds, or cherry pick development projects in their countries. By utilizing KIVA, we have the ability to pick our own partners and projects in order to ensure that our funds are well managed, put in the hands of individuals that want to enhance their lives, and produce results that can be passed on to the next generation.

The initiative was also introduced simultaneously to the Political Science and Public Administration departments, both of which were glad to get involved. Professor Holly Jarman enlisted the help of her colleagues and with the help of class members pitched the idea to a class in Public Administration that, after assurance that future years would also donate and raise funds also joined the effort. Thus began the endeavor to enlist donations. With a goal of $300, emails were sent to professors, and some face-to-face groundwork was carried out in getting staff on board with the idea. At this point, we had done what could be considered the easy part of the ordeal. We still needed to decide which partner organizations, what types of projects we would consider donating to and how much to give to each. The class then dedicated time to ironing out the details of unwanted traits of partner organizations, and key things we wanted to pay special attention to. We concluded that each member of the class would take a subregion, as divided by the Kiva’s website. We did not want to invest in organizations that required their loan beneficiaries to partake in religious activities as a stipulation, and we did not want organizations whose values undermined the basic values of projects like this. The class decided that preferable were organizations with similar core values to the University at Albany, ones that had lengthier track records on Kiva, had high repayment rates, low comparative interest rates and did not engage in external activity antithetical to the aforementioned core values. Finally, the class wanted to invest in a variety of organizations so that by the time the next generation of students would be working on Kiva, they might be able to see some of the returns.

Next, the class narrowed down their results by region. This was extremely challenging because Kiva relies upon its partner organizations to report local indicators. This naturally compromised the reliability of the figures. Regionally, Eastern Europe had a scant listing of organizations. Asia had the most successful organizations by rate of repayment (90% and above), whereas the other regions hovered within the 80% range. Our meeting revealed that narrowing down a top 5 set of organizations was difficult because in some instances, we wanted to give a chance to pilot organizations but were fearful of our donors feeling insecure in such an investment. In other instances, we liked the established organizations but an examination of their websites revealed an overly capitalist project (i.e. long polished wooden board room tables with businessmen in interviews that consistently mentioned how “profitable” they were, which cast a slightly negative feeling. To our surprise, our initial concern that women would not be represented was completely countered by the fact that almost all the organizations made above 50% of their loans to women. During two hours of discussion, the class decided to narrow their short list of 5 to an even shorter list of 3 by region. We posted these to our class website, and joined the Kiva Group Membership Dr. Jarman had created on the Kiva website. On the last day of class, we were informed that the Initiative had raised $800 dollars. Having exceeded our goal, the money was split between the political science and public administration classes to be donated accordingly. In the coming years it is our hope that students will engage as thoroughly and unreservedly by gathering donations and actively carrying on this project. It is our hope that by encouraging an entrepreneurial spirit, and raising the standard of living directly for individuals that have the drive and ambition to engage in development in some of the least developed countries, that in some way we are helping them transition to a modern economy one business at a time. This initiative is an embodiment of the world within reach.

What we did and why we did it

The Rockefeller College Microfinance Initiative began as an idea generated from the Spring 2009 Foreign Economic Policy class. The challenges of development and the hardships of global poverty inspired a drive to get involved as a unit, as well as on behalf of the College. While noting its shortcomings, the class elected to get involved in microfinance and the decision was made to use Kiva.org as the institution through which the investment would be made. The microfinance or micro loan model of aid has a much different structure to foster a higher standard of living for individuals living in poverty. These programs provide money, but in the form of loans rather than goods or services. These loans are given to entrepreneurs that can use the money to invest in their own production capacity. They invest in projects ranging from business investment for expansion, agricultural production, or whatever project that will generate income so that the loan can be repaid and passed on to the next project. Thus, Kiva was a good fit for our initiative. One of the best traits of microfinance projects is that the individuals involved are in charge of their own destiny. They are taking on risk, just the same as the donor is taking a risk of not having their loan repaid. There are also added benefits of bypassing many government agencies that could potentially divert funds, or cherry pick development projects in their countries. By utilizing KIVA, we have the ability to pick our own partners and projects in order to ensure that our funds are well managed, put in the hands of individuals that want to enhance their lives, and produce results that can be passed on to the next generation.

The initiative was also introduced simultaneously to the Political Science and Public Administration departments, both of which were glad to get involved. Professor Holly Jarman enlisted the help of her colleagues and with the help of class members pitched the idea to a class in Public Administration that, after assurance that future years would also donate and raise funds also joined the effort. Thus began the endeavor to enlist donations. With a goal of $300, emails were sent to professors, and some face-to-face groundwork was carried out in getting staff on board with the idea. At this point, we had done what could be considered the easy part of the ordeal. We still needed to decide which partner organizations, what types of projects we would consider donating to and how much to give to each. The class then dedicated time to ironing out the details of unwanted traits of partner organizations, and key things we wanted to pay special attention to. We concluded that each member of the class would take a subregion, as divided by the Kiva’s website. We did not want to invest in organizations that required their loan beneficiaries to partake in religious activities as a stipulation, and we did not want organizations whose values undermined the basic values of projects like this. The class decided that preferable were organizations with similar core values to the University at Albany, ones that had lengthier track records on Kiva, had high repayment rates, low comparative interest rates and did not engage in external activity antithetical to the aforementioned core values. Finally, the class wanted to invest in a variety of organizations so that by the time the next generation of students would be working on Kiva, they might be able to see some of the returns.

Next, the class narrowed down their results by region. This was extremely challenging because Kiva relies upon its partner organizations to report local indicators. This naturally compromised the reliability of the figures. Regionally, Eastern Europe had a scant listing of organizations. Asia had the most successful organizations by rate of repayment (90% and above), whereas the other regions hovered within the 80% range. Our meeting revealed that narrowing down a top 5 set of organizations was difficult because in some instances, we wanted to give a chance to pilot organizations but were fearful of our donors feeling insecure in such an investment. In other instances, we liked the established organizations but an examination of their websites revealed an overly capitalist project (i.e. long polished wooden board room tables with businessmen in interviews that consistently mentioned how “profitable” they were, which cast a slightly negative feeling. To our surprise, our initial concern that women would not be represented was completely countered by the fact that almost all the organizations made above 50% of their loans to women. During two hours of discussion, the class decided to narrow their short list of 5 to an even shorter list of 3 by region. We posted these to our class website, and joined the Kiva Group Membership Dr. Jarman had created on the Kiva website. On the last day of class, we were informed that the Initiative had raised $800 dollars. Having exceeded our goal, the money was split between the political science and public administration classes to be donated accordingly. In the coming years it is our hope that students will engage as thoroughly and unreservedly by gathering donations and actively carrying on this project. It is our hope that by encouraging an entrepreneurial spirit, and raising the standard of living directly for individuals that have the drive and ambition to engage in development in some of the least developed countries, that in some way we are helping them transition to a modern economy one business at a time. This initiative is an embodiment of the world within reach.

More recipients

Pictured here are Jonathan Omege from Benin City in Nigeria, Le Thi Vinh from Hung Nguyen in Viet Nam, and the J/kheri Groupfrom Darajabovu in Tanzania, who have received money from our fund.

What we did, part I - RPOS 572, Spring 2009

TO: Future Micro-Finance Project Leaders

FROM: Michael Dutt

SUBJECT: My Experience

SUMMARY: The idea behind using an aid mechanism such as microfinance in order to provide help to individuals in depressed economic situations around the world is to not only provide the necessary funding for individual development, but to create a sustainable aid program that can be continued by the next generation of students. There are also added benefits of bypassing many government agencies that could potentially divert funds, or cherry pick development projects in their countries. By utilizing KIVA, we have the ability to pick our own partners and projects in order to ensure that our funds are well managed, put in the hands of individuals that want to enhance their lives, and produce results that can be passed on to the next generation.

Many of the donations that I have made in the past are simply monetary contributions that are made with the hope that the organization will put the funds to good use, and produce programs that help the needy. In many cases these programs are simply providing services that individuals need in order to raise their standard of living, with no real effort needed by the recipient. This model of aid has worked well for the vast majority of non-profits, and NGO’s that provide these services.

The microfinance or micro loan model of aid has a much different structure to foster a higher standard of living for individuals living in poverty. These programs do provide money, but in the form of loans rather than goods or services. These loans are given to entrepreneurs that can use the money to invest in their own production capacity. They invest in projects ranging from business investment for expansion, agricultural production, or whatever project that will generate income so that the loan can be repaid and passed on to the next project.

One of the best traits of microfinance projects is that the individuals involved are in charge of their own destiny. They are taking on risk, just the same as the donor is taking a risk of not having their loan repaid. The stakes are high for these individuals, and we are giving them the tools they need to help themselves. Simply providing aid in the form of food, or other forms of care can raise the standard of living for an individual for a period of time, but helping these individuals develop their own systems to generate income has the potential to provide a lifetime of benefits.

It is my hope that encouraging an entrepreneurial spirit, and raising the standard of living directly for individuals that have the drive and ambition to pull themselves up by their own bootstraps will have the wide ranging benefit of fostering growth in some of the least developed countries, and helping them transition to a modern economy one business at a time. Want to change the world?

FROM: Michael Dutt

SUBJECT: My Experience

SUMMARY: The idea behind using an aid mechanism such as microfinance in order to provide help to individuals in depressed economic situations around the world is to not only provide the necessary funding for individual development, but to create a sustainable aid program that can be continued by the next generation of students. There are also added benefits of bypassing many government agencies that could potentially divert funds, or cherry pick development projects in their countries. By utilizing KIVA, we have the ability to pick our own partners and projects in order to ensure that our funds are well managed, put in the hands of individuals that want to enhance their lives, and produce results that can be passed on to the next generation.

Many of the donations that I have made in the past are simply monetary contributions that are made with the hope that the organization will put the funds to good use, and produce programs that help the needy. In many cases these programs are simply providing services that individuals need in order to raise their standard of living, with no real effort needed by the recipient. This model of aid has worked well for the vast majority of non-profits, and NGO’s that provide these services.

The microfinance or micro loan model of aid has a much different structure to foster a higher standard of living for individuals living in poverty. These programs do provide money, but in the form of loans rather than goods or services. These loans are given to entrepreneurs that can use the money to invest in their own production capacity. They invest in projects ranging from business investment for expansion, agricultural production, or whatever project that will generate income so that the loan can be repaid and passed on to the next project.

One of the best traits of microfinance projects is that the individuals involved are in charge of their own destiny. They are taking on risk, just the same as the donor is taking a risk of not having their loan repaid. The stakes are high for these individuals, and we are giving them the tools they need to help themselves. Simply providing aid in the form of food, or other forms of care can raise the standard of living for an individual for a period of time, but helping these individuals develop their own systems to generate income has the potential to provide a lifetime of benefits.

It is my hope that encouraging an entrepreneurial spirit, and raising the standard of living directly for individuals that have the drive and ambition to pull themselves up by their own bootstraps will have the wide ranging benefit of fostering growth in some of the least developed countries, and helping them transition to a modern economy one business at a time. Want to change the world?

Our first loan recipient!

We have made our first loan - to Khun Sokha in Cambodia. I'll be posting updates on each of the loans as soon as they are made. A big thank you to all of our donors!

Subscribe to:

Posts (Atom)